Article Directory

So the headlines are screaming it from the digital rooftops: "Mortgage Rates Hit One-Year Low!" You can almost hear the triumphant trumpets and see the confetti falling. Lenders are practically begging you to look at their shiny new 6.19% rate for a 30-year fixed loan. A whole percentage point lower than the soul-crushing 7% we saw at the start of 2025.

Give me a break.

Are we supposed to throw a parade because the cost of borrowing a life-altering amount of money is merely "exorbitant" instead of "catastrophic"? This isn't a gift. It's a slightly less-painful punch to the gut. Let's get real about what this "news" actually means for anyone who doesn't work on Wall Street.

The So-Called "Good News"

I'm staring at this quote from Sam Khater, Freddie Mac’s chief economist, who says this dip has "kept refinancings high." High? High compared to what, exactly? The last few months when rates were so terrifying that only lottery winners were buying houses? Offcourse it's higher than that.

The real story, the one buried under all the self-congratulatory press releases like Mortgage and refinance interest rates today, October 24, 2025: Now at a more than a one-year low, is that this "low" rate is still a complete joke to the overwhelming majority of American homeowners. Remember that little global event a few years back? The one that let the government pump the economy full of cash and sent mortgage rates plummeting to the 2s and 3s? Yeah, people remember. A report from Redfin not too long ago showed that something like 83% of homeowners with a mortgage are sitting on a rate below 6%. Over half are paying less than 4%.

So who, precisely, is this "good news" for? Is it for the millions of us locked into our golden handcuffs, unable to move because selling our 3.25% mortgage home for a new one at 6.19% would be financial suicide? Or is it for the tiny, unfortunate sliver of the population who bought a house in the last 18 months and got absolutely hosed with a 7%+ rate? I guess for them, this is a relief. But celebrating this feels like celebrating that the house fire was downgraded to a three-alarm blaze instead of a four-alarm one. The house is still on fire.

The Banker's Shell Game

Let's not forget the fine print. Refinancing isn't some magic button you press to lower your payment for free. It’s a whole new loan application, complete with all the fees the banks love to tack on. We’re talking closing costs of 2% to 6% of your loan amount. On a $400,000 mortgage, that’s anywhere from $8,000 to $24,000 out of your pocket, just for the privilege of shuffling some paperwork.

The whole system is a carefully constructed casino where the house always wins. When rates are high, they make a killing on interest. When rates dip slightly, they lure you into a refinance and make a killing on origination fees and closing costs. It's a beautiful grift. It reminds me of trying to pay my utility bill online and getting hit with a $3 "convenience fee." Convenient for who? It sure as hell ain't convenient for me. It's just another way to extract a few more bucks from you because they can.

This whole song and dance is just that—a distraction. They want you focused on the shiny object, the "lowest rate in a year," so you don't think too hard about the underlying game. This is a bad deal. No, 'bad' doesn't cover it—this is a five-alarm dumpster fire of a financial landscape, and they're handing us a thimble of water and calling themselves heroes.

So, What's the Play?

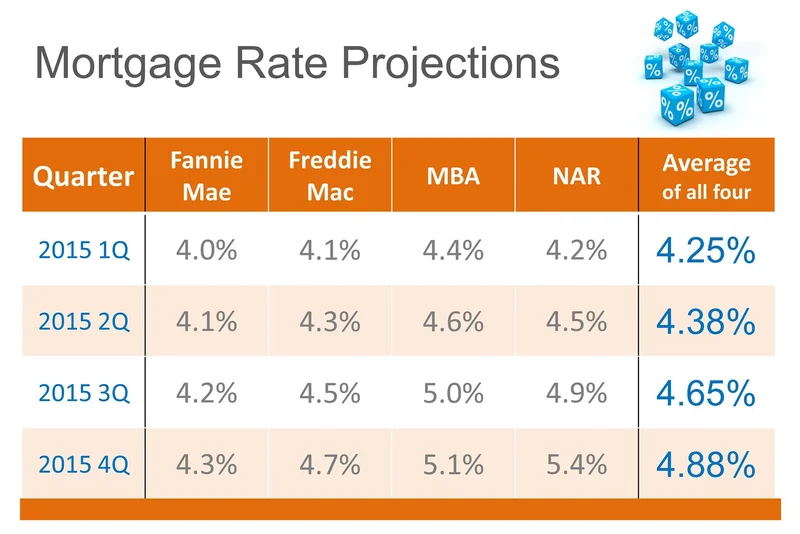

If you're looking for a silver lining, you'll have to squint pretty hard. The forecasts from the big shots at Fannie Mae and the Mortgage Bankers Association don't exactly paint a rosy picture. They're predicting rates will stay bobbing around the 6% mark for most of 2026. This isn't a dip; it's the new plateau. The idea that we'll ever see 3% again is a collective fantasy we need to let go of, and honestly...

The Federal Reserve is cutting its benchmark rate, sure, but that’s not a guarantee of anything. We saw them cut rates last fall, and mortgage rates just laughed and climbed higher anyway. With the current administration's love for tariffs and trade wars, who knows what inflation will do next? The economy feels like a Jenga tower where someone just pulled a critical block from the bottom. We're all just holding our breath, waiting for the crash.

Then again, maybe I'm the crazy one here. For that person who bought their first home last January at 7.2%, refinancing to 6.2% could save them hundreds of dollars a month. That's real money that could go to groceries or daycare. I get it. But it feels like we’ve lowered the bar so far that we’re celebrating mediocrity. We're so beaten down by a hostile market that a slightly less terrible deal feels like a victory.

Don't Pop the Champagne Just Yet

Look, this isn't a recovery. It's a dead cat bounce for a housing market that's been in a coma. For the vast majority of homeowners, this "lowest rate in a year" is completely irrelevant noise. It’s a headline for the banks, by the banks. The real story isn't that rates are falling from an insane peak to a merely terrible level. The real story is that the golden age of cheap money is over, and it ain't ever coming back. Don't let them fool you into thinking this is a party. It's just a slightly more decorated prison cell.